Unabsorbed mat credit will be allowed to be.

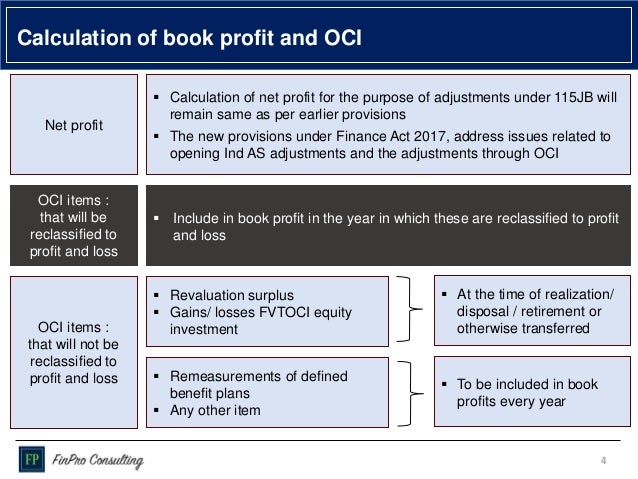

Meaning of book profit for mat computation.

The mat provisions begin with a non obstante clause and thus are a sacrosanct and self contained code.

Means the tax payable on the basis of normal computation of total income of the company.

Calculation of book profits for the purpose of mat maximum alternate tax section 115jb for computation of book profit one may proceed as follows.

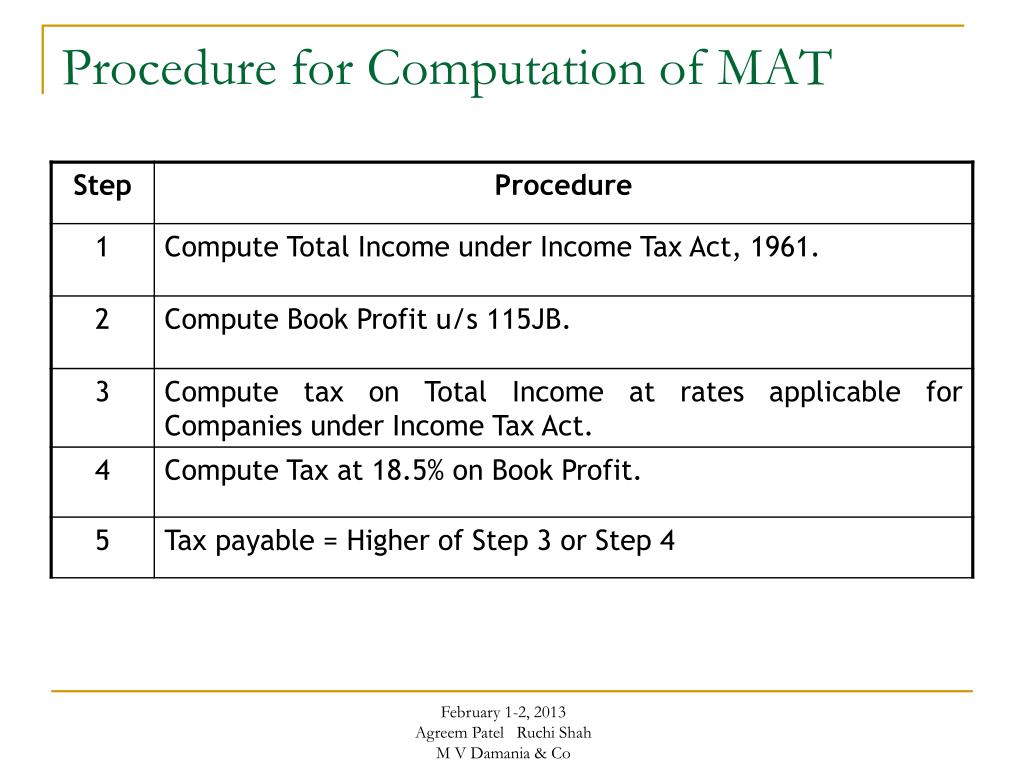

How to calculate mat.

Mat provisions require book profit to be adjusted against lower of brought forward unabsorbed loss and unabsorbed depreciation and not merely restrict the amount set off to the lower number august 21 2018 in brief in a recent ruling1 of the ahmedabad bench of the income tax appellate tribunal tribunal an issue.

Computation of book profit.

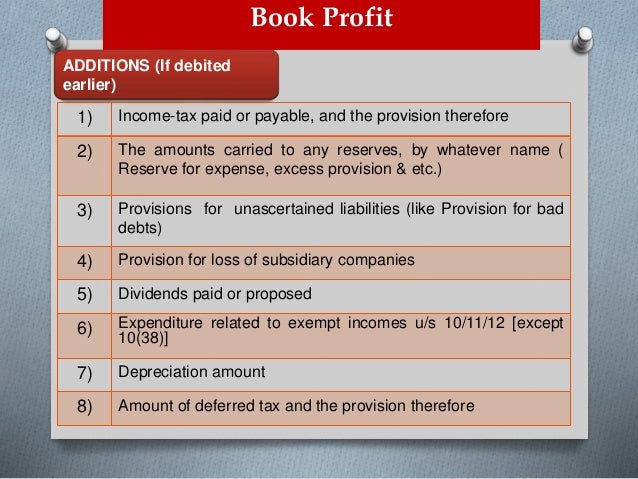

Additions to the net profit if debited to the profit and loss account.

Mat is levied at the lower rate of 9 plus surcharge and cess as applicable for companies that are a unit of an international financial services centre and derive their income solely in.

In other words the mat provisions in section 115jb create a deeming fiction which deems book profit as the total income of a company for determining its tax liability.

Mat credit will be allowed to carry forward facility for a period of 10 assessment years immediately succeeding the assessment year in which mat is paid.

Minimum alternate tax mat.

A the amount of income tax paid or payable and the provision thereof.

Book profit means the net profit as shown in the profit loss account for the year as increased and decreased by the following items.

In other words it refers to money earned by an entity during a financial year by selling products and services deducted by all the expenses incurred during the same financial year.

We can define book profit as the leftover money after the entity pays off all its expenses and as shown in the statement of profit and loss.

Book profits as per section 115jb 1 01 00 000.

For fy 2019 20 tax payable is computed at 15 previously 18 5 on book profit plus applicable cess and surcharge.

The net profit as shown in the profit and loss account prepared as per part ii and iii of schedule vi for the relevant fy shall be increased by the following if debited to the profit and loss accounts.

Mat is equal to 18 5 15 from ay 2020 21 of book profits plus surcharge and cess as applicable.